IRS Requirements For 1031 Exchanges

IRS Requirements For 1031 Exchanges

Couldn't load pickup availability

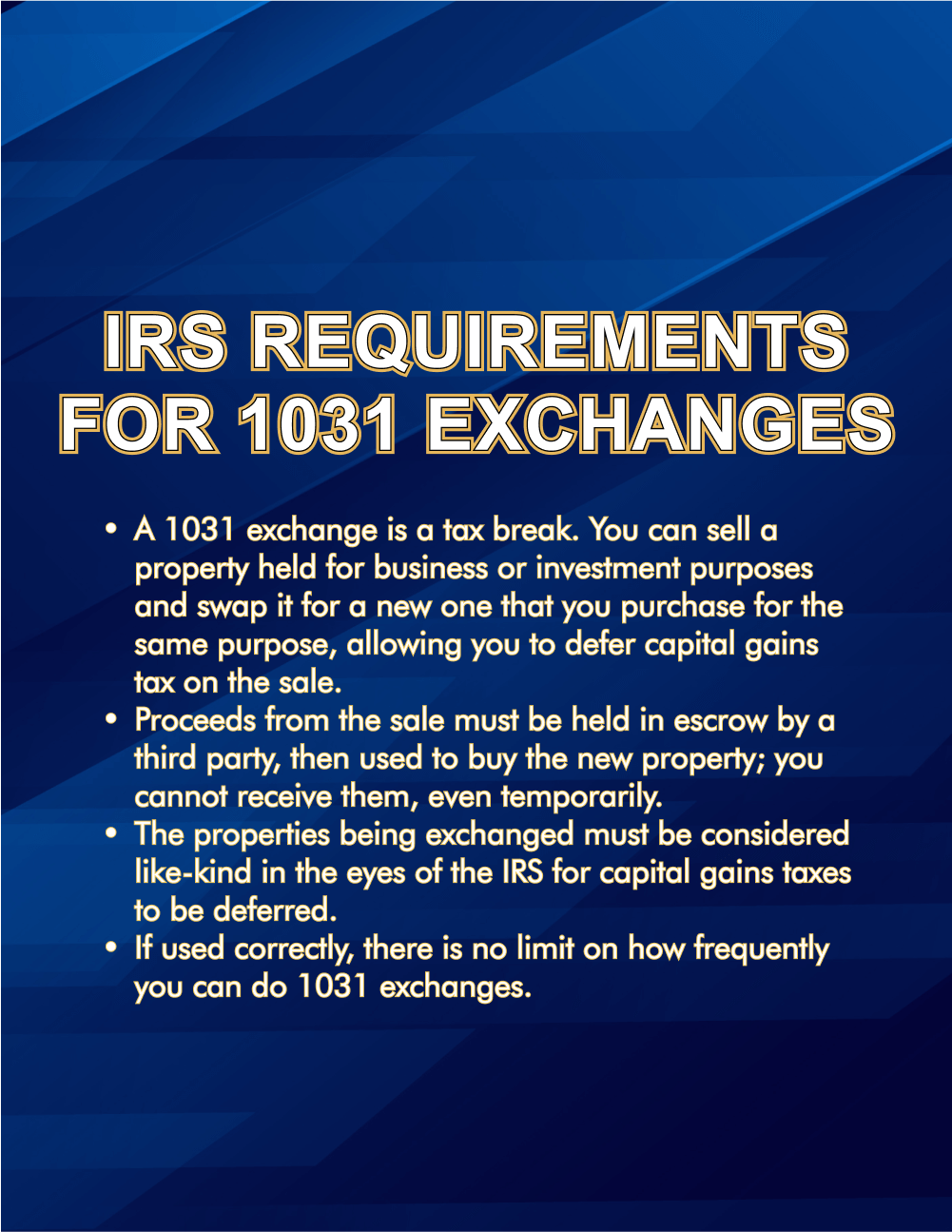

IRS requirements for 1031 exchanges are important for real estate investors who want to legally defer capital gains taxes when selling and reinvesting in another investment property. A 1031 exchange, named after Section 1031 of the Internal Revenue Code, allows investors to exchange one qualifying property for another while postponing tax obligations. However, to benefit from this strategy, investors must strictly follow the IRS guidelines governing these transactions.

One of the key IRS requirements for 1031 exchanges is the timeline rule. After selling the original property, investors have 45 days to identify potential replacement properties and 180 days to complete the purchase of the new investment property. Missing these deadlines can disqualify the exchange and result in immediate tax liability.

Another important requirement involves the use of a qualified intermediary. The investor cannot receive or control the sale proceeds directly. Instead, a qualified intermediary must hold the funds and facilitate the transaction between both property exchanges. Additionally, the properties involved must be considered like-kind, meaning they are both used for investment or business purposes.

Understanding the IRS requirements for 1031 exchanges helps investors structure property transactions correctly, protect their capital, and grow their real estate portfolios while remaining fully compliant with federal tax regulations. Proper planning and knowledge of these rules can make 1031 exchanges one of the most powerful tax-deferral strategies available to real estate investors.